Employers Need a Better Formulary to Deliver Rx Value and Savings

Americans spend about $500 billion a year on prescription drugs with no visibility into the processes that set prices or the comparative effectiveness of drugs approved for the same clinical purpose. This opaqueness makes it impossible to ensure that prices are aligned with the value a drug provides.

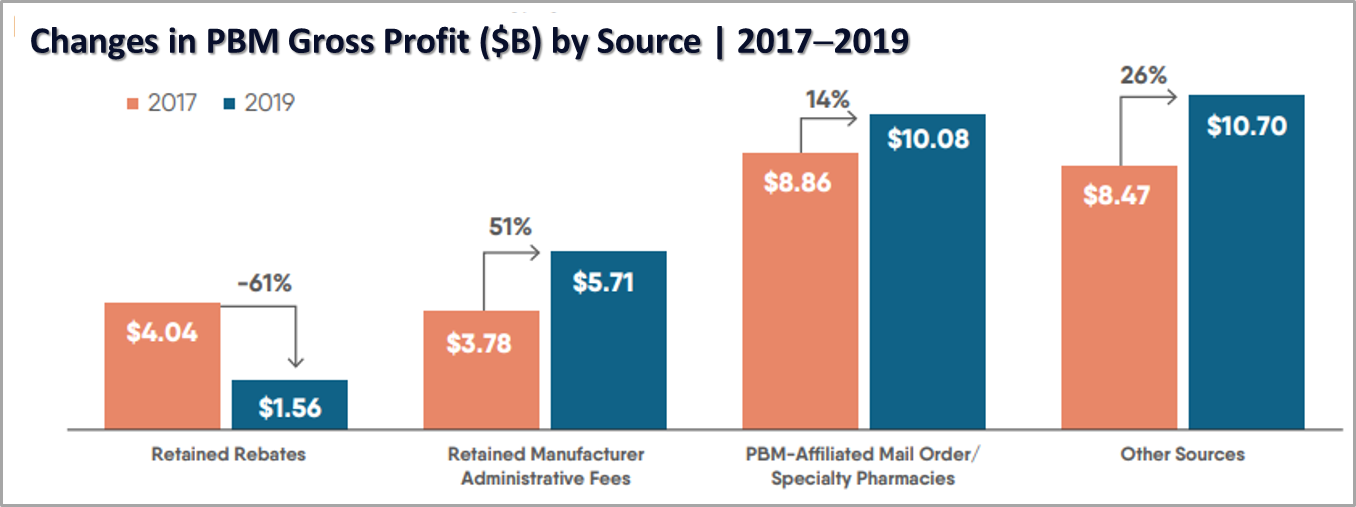

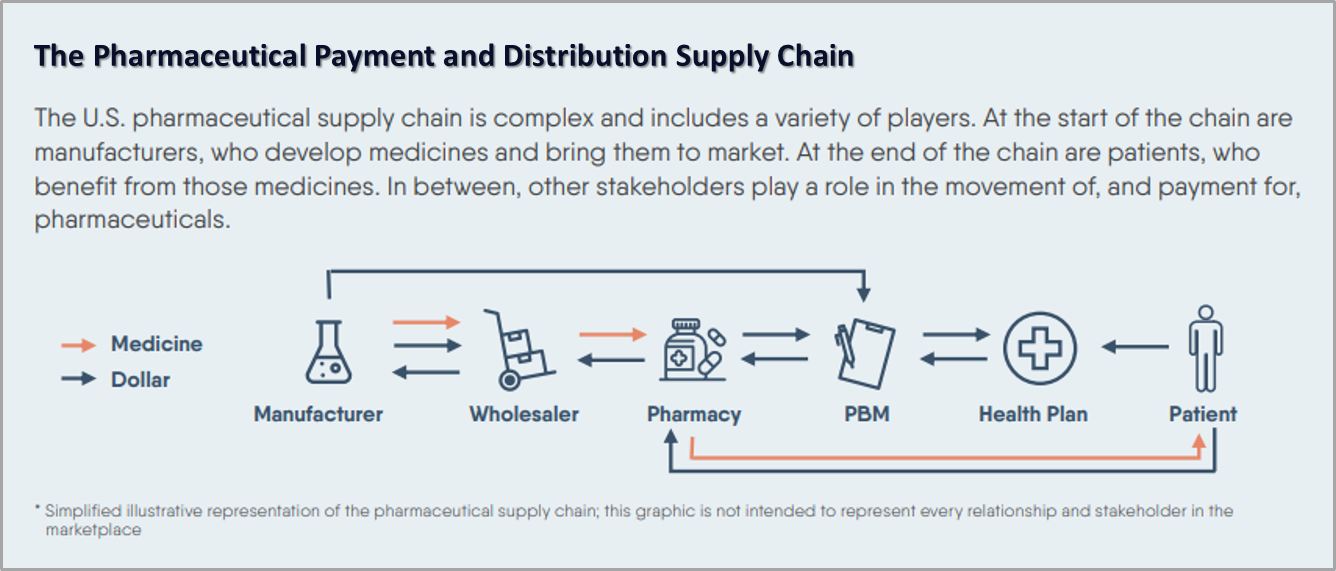

PBMs are primarily responsible for this lack of transparency by adding cost through spread pricing and creating drug formularies based on the rebates they receive from manufacturers. The good news for employer health plan sponsors and their members is that some researchers are trying to change this.

In their review of research by the Center for Evaluation of Value and Risk in Health at Tufts Medical Center, Health Affairs notes that there is no single entity in the U.S. that makes drug coverage and pricing decisions. This is compounded by the mix of private and public payers that follow different rules, and a system that grants monopolies to drug manufacturers and allows them to charge whatever the market will bear.

A Way Forward

The way out of this mess is to build prescription drug formularies that consider comparative effectiveness research and cost. The researchers support the science-driven approach that is advocated by the Institute for Clinical and Economic Review (ICER) and is used by next-generation Rx plans to deliver better value and better outcomes.

ICER is an independent, non-profit research organization founded in 2006 at Harvard Medical School. It evaluates the clinical and economic value of prescription drugs, medical tests and devices, and health system delivery innovations. ICER believes that when drug pricing reflects how well the drug improves patients’ lives, it will incentivize transformational innovation by rewarding pharmaceutical companies for developing more highly effective drugs. Without such philosophical and economic shifts, Americans will continue to pay too much for drugs that do too little.

ICER has developed a recommended health-benefit price benchmark (HBPB) for U.S. drug prices, net of rebates and discounts. This is certainly a step in the right direction but as we know, rebates and other PBM practices are little more than a scam. Additionally, of all the drugs ICER has assessed, only slightly more than 25% were priced within their HBPB range.

Brokers and advisors can empower employers by offering prescription drug plans that deliver value based on cost and comparative clinical efficacy. It’s time to replace the predatory practices and overriding profit motive of PBMs with formularies that prioritize drugs offering the best overall value based on comparative data, next-generation payment technology, smart sourcing, and evidence-based improvements in patient outcomes and savings.

Contact Vitori Health for information about our non-PBM VitoriRx plan that does all this and more.