How to Win the War for Talent with Better Employee Health Benefits

The war for talent has escalated thanks to “The Great Resignation,” a pandemic-driven trend in which employees are quitting their jobs in record numbers. While some change careers, most seek new positions that better align with their priorities, which include higher pay and better health benefits.

This level of churn is exhausting, expensive, and disruptive. Consider that 44% of employees are “job seekers” and of them, 33% are active “job hunters,” according to the 2022 Global Benefits Attitudes Survey conducted by WTW (Willis Towers Watson).

Additionally, Gallup estimates that “The cost of replacing an individual employee can range from one-half to two times the employee’s annual salary. So, a 100-person organization that provides an average salary of $50,000 could have turnover and replacement costs of approximately $660,000 to $2.6 million per year.”

Clearly, this is not sustainable.

The Importance of Cost-Effective Health Benefits

Although making more money is often the top reason for changing jobs, a CNBC analysis of the WTW survey identifies health benefits as the #2 reason why “almost 20% said they’d take a new job for the same pay — suggesting factors other than wages are important, too.”

The WTW survey affirms this. “Benefits packages that meet the needs of employees and provide an enhanced experience result in significantly greater retention (78% vs 41% when the benefits package does not meet the needs).”

Employers competing for top talent should consider replacing high-cost, traditional health plans with innovative plans that challenge and transcend the byzantine practices of insurers, PBMS, and health systems. Decisive steps can be taken today to offer enhanced health benefits that deliver better access to care at lower, more realistic costs for employers and employees.

Employees Have Responsibilities Too

It’s one thing for employees and job seekers to demand better health benefits. It’s another to take responsibility for personal finances by fully understanding everything offered by a health plan.

The Wall Street Journal asserts that the best time to evaluate plan options is during open enrollment. When confronted with thick booklets and lengthy documents, many employees make quick, simple choices instead of exploring the potential value of more complex plan options. This is a missed opportunity to save money and secure the most appropriate coverage for their family.

It also prevents employees from evaluating whether certain benefits are worth the cost. While employers have been ramping up benefits in the war for talent, inflation has made consumers more cost sensitive. Employees can reduce monthly paycheck deductions and increase satisfaction with their health plan by choosing only those benefits that best support them, especially during the continued and evolving pandemic.

A Sustainable Benefits Future

In the war for talent, health plans that offer better health benefits at a lower cost have a clear competitive advantage. When companies save 30% on health plan spending without cost shifting, they can redirect those funds to what employees and candidates seek: higher salaries and signing bonuses, increased direct and indirect compensation, and enhanced employment amenities. And there’s an immediate and significant improvement to the balance sheet that can catapult a business ahead of its competition.

Employees are demanding health benefits beyond the status quo as they move from job to job. Employers can make that happen by offering a better health plan experience and helping employees evaluate their options during open enrollment.

Now that’s sustainable!

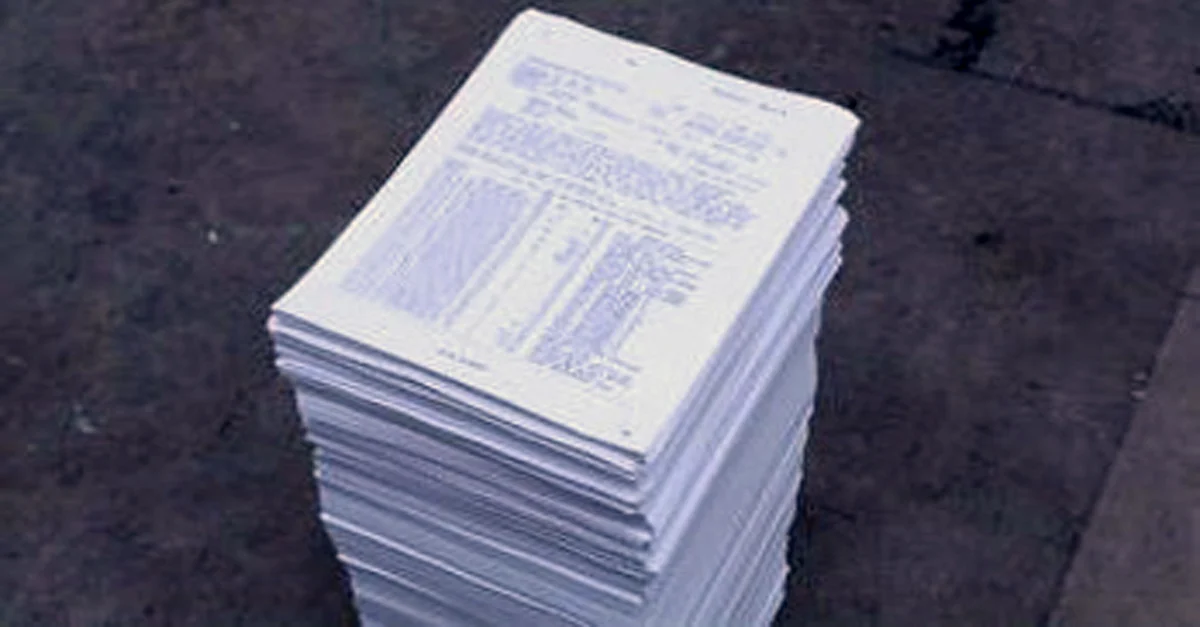

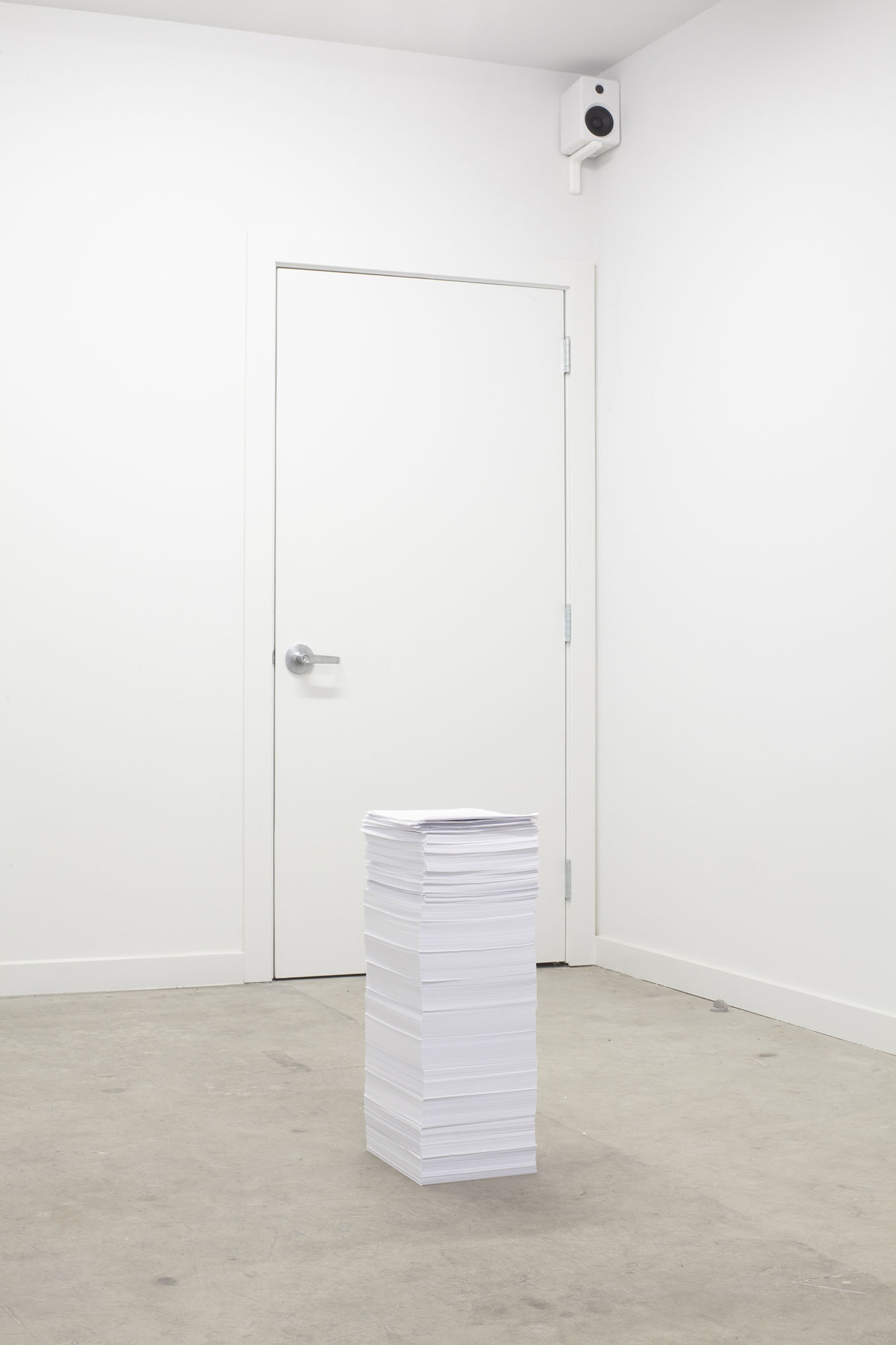

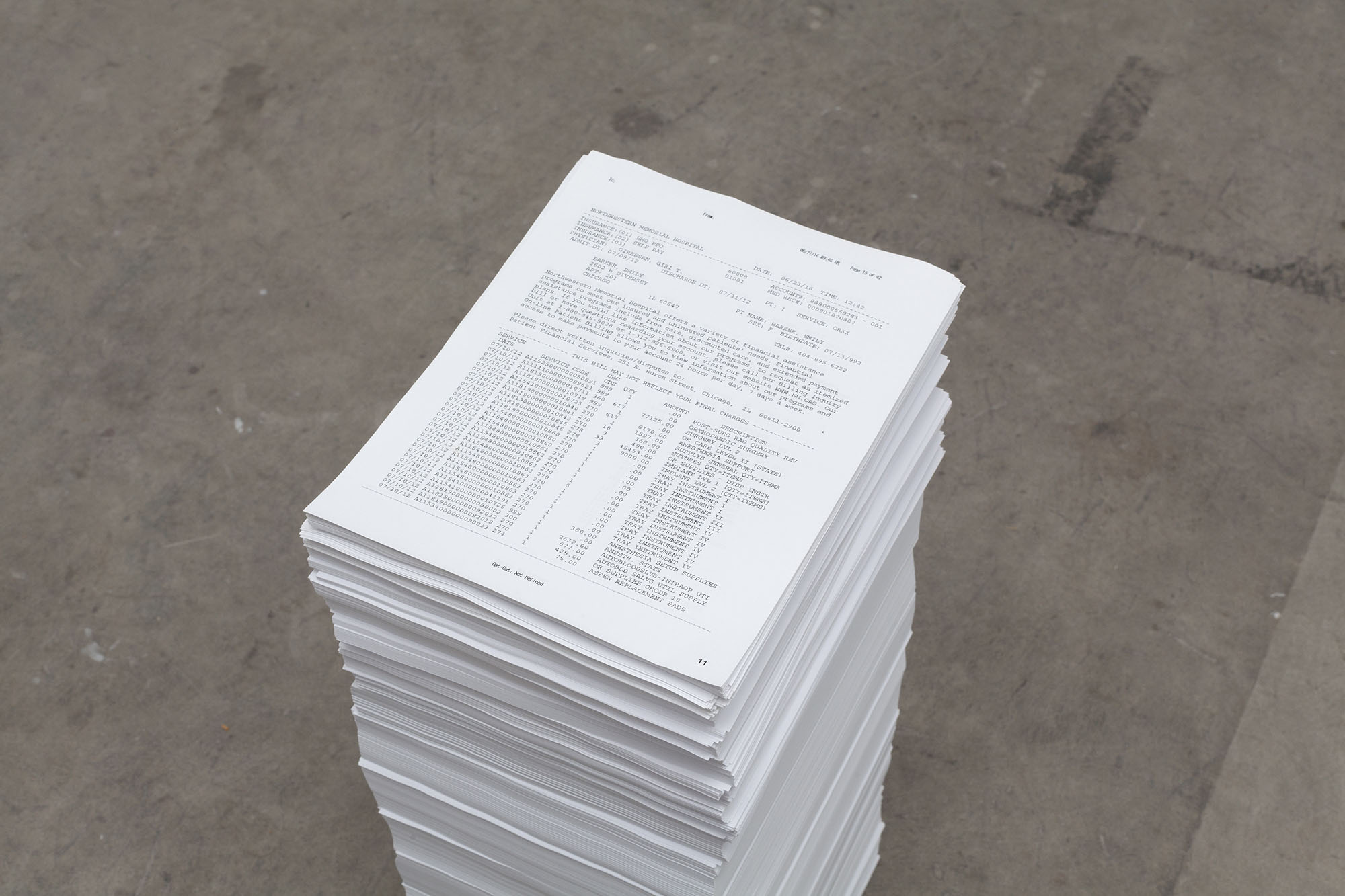

This installation-based work is a neat pile of 7,865 documents from 2012 to 2015 that includes bills for medical treatments, medical records, and care plans with their accompanying costs. Had all communications with the bureaucracy of the healthcare system to date been included, the pile would have fallen over.

This installation-based work is a neat pile of 7,865 documents from 2012 to 2015 that includes bills for medical treatments, medical records, and care plans with their accompanying costs. Had all communications with the bureaucracy of the healthcare system to date been included, the pile would have fallen over. Note the piece of paper on top of the pile: a partial bill from the day after the accident in excess of $144,000 for various surgical interventions on Barker’s spinal cord.

Note the piece of paper on top of the pile: a partial bill from the day after the accident in excess of $144,000 for various surgical interventions on Barker’s spinal cord.