WATCH | Health Plan Funding Options: Financial Facts and Fables

< 1 minute

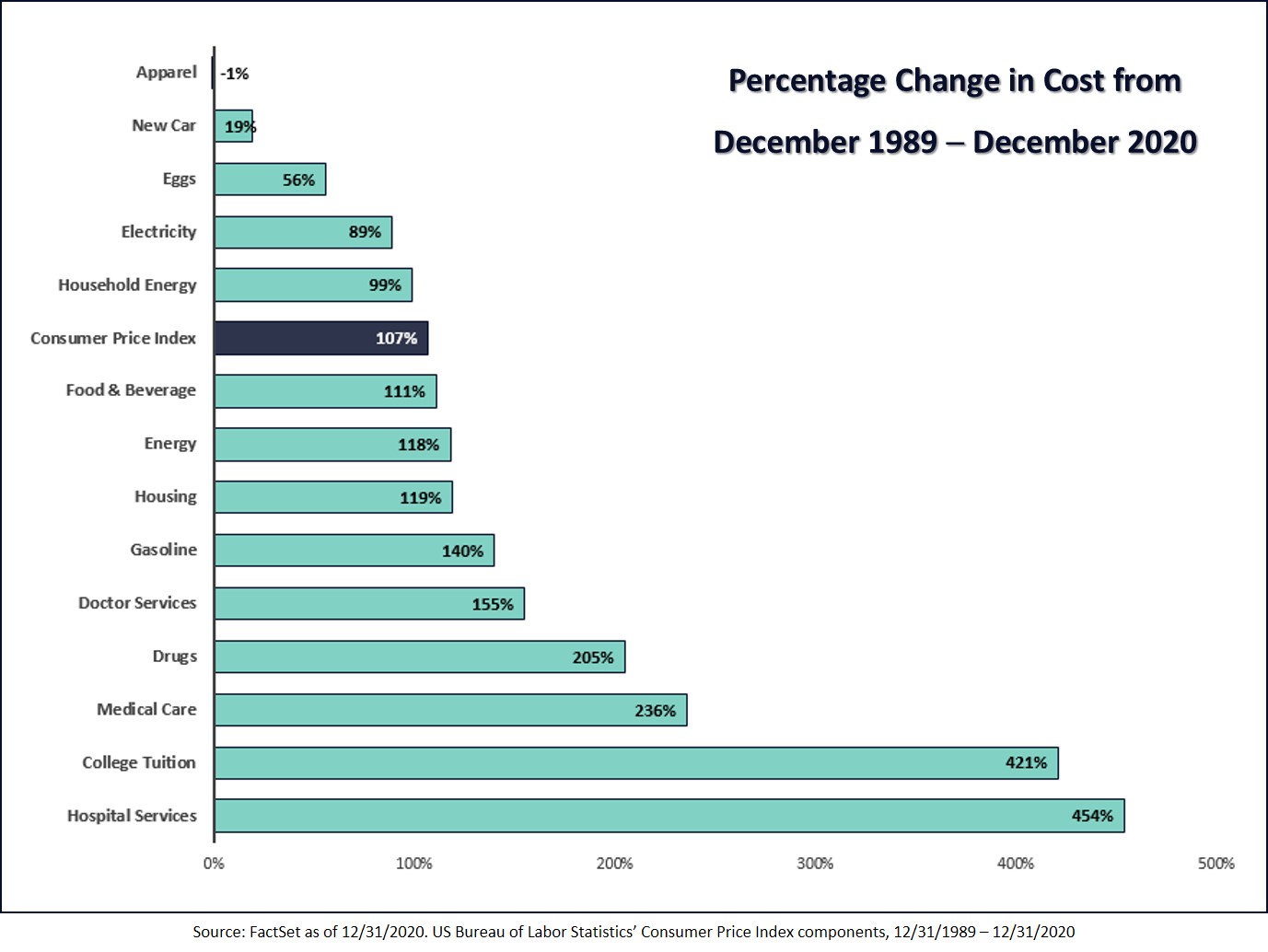

It’s not always apparent that the ability to control costs is directly impacted by how an employee health plan is funded. From fully-funded to self-insured, choosing the right insurance model is key to optimizing reimbursement and maximizing value and savings.

Brokers and employers can benefit from having a deeper understanding of risk transfer and health plan funding. Without such clarity, it can be difficult to establish insurance arrangements that optimize cost control.

Watch our fast-moving, 30-minute on-demand webinar to acquire the information you need to:

- Know the gradations of fund planning and their respective pros and cons

- Understand why fully-insured plans typically offer minimal cost controls

- Realize that self-funding is appropriate for employers of all sizes

- Learn how to maximize savings and value with a high performance health plan

- Estimate current overspending and cost-saving opportunities

Watch now and contact Vitori Health for personalized insights into shaping and influencing an optimized health plan.

Vitori’s focus for the next few years will be growing its revenue and customer base and scaling its business nationwide. According to O’Brien, “We have found strong initial success, with client plan members in 48 states. And we’ve seen strong interest from brokers and advisors looking to save costs for their self-insured client health plans.”

Vitori’s focus for the next few years will be growing its revenue and customer base and scaling its business nationwide. According to O’Brien, “We have found strong initial success, with client plan members in 48 states. And we’ve seen strong interest from brokers and advisors looking to save costs for their self-insured client health plans.”

We are therefore delighted to introduce our new CEO,

We are therefore delighted to introduce our new CEO,